ASML Holding (ASML) Hold Thesis Brief

Sector Classification: Semiconductor Manufacturing Equipment

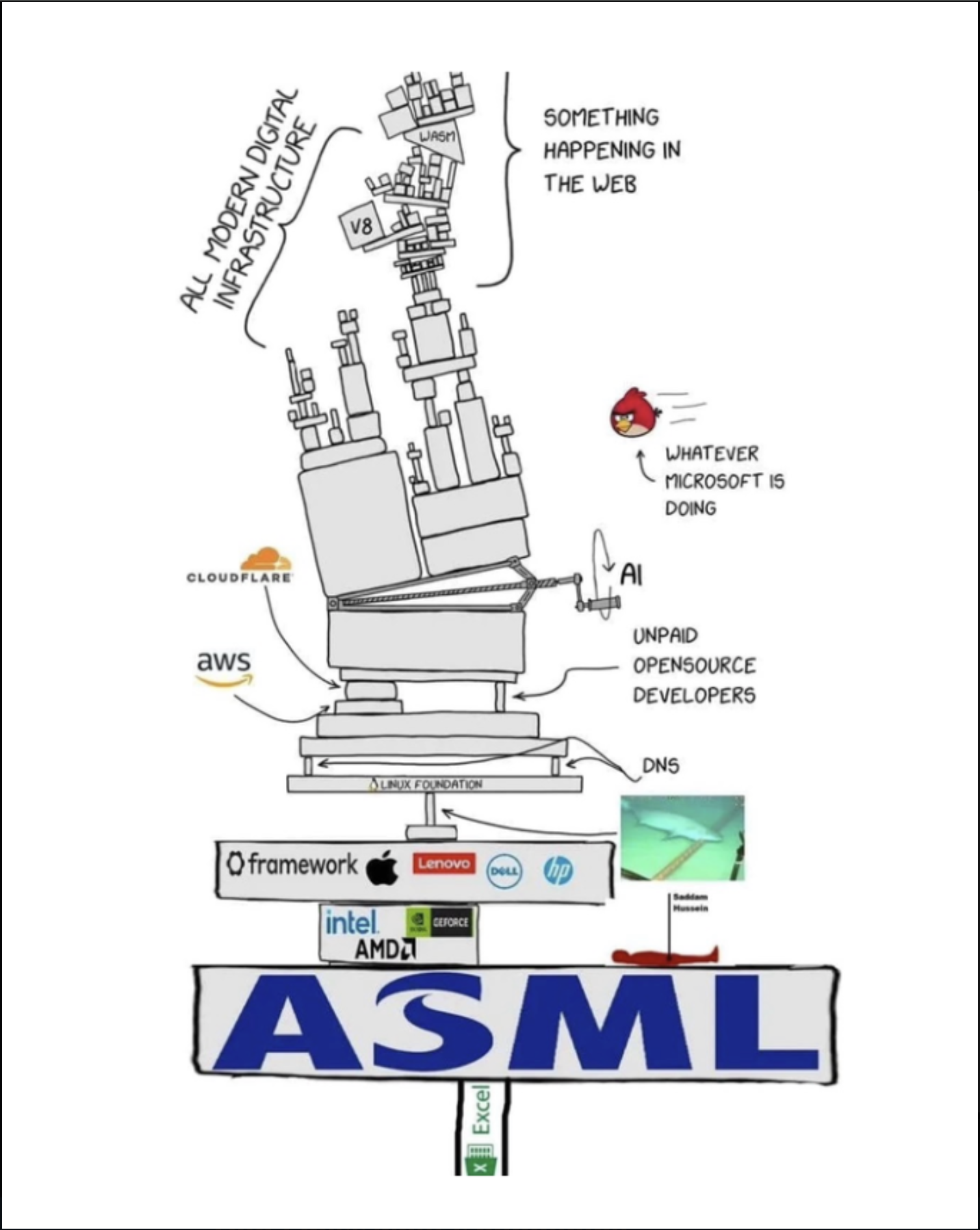

Layer: Chip Manufacturing (the machines that make the chips)

Verdict: Buy and hold. ASML is a true monopoly on the single most important machine in the modern economy. This is a position to own for years and add to on dips, not to trade.

Why I Own It (Plain English)

Every advanced computer chip in the world (the ones powering AI, phones, data centers) is made using a process called lithography, which is essentially printing unimaginably tiny patterns onto silicon. The most advanced version of this is called EUV (extreme ultraviolet) lithography, and ASML is the only company on Earth that makes EUV machines. Not the best, the only.

If a chipmaker like TSMC, Samsung, Intel, or SK Hynix wants to make a cutting-edge chip, they have no choice but to buy from ASML. There is no competitor. These machines cost hundreds of millions of dollars each, take years to build, contain hundreds of thousands of parts, and require a global supply chain that took decades to assemble. No one can simply decide to compete with ASML; the barrier to entry is one of the widest in the entire economy.

The simple way to think about it: in the AI gold rush, everyone is buying picks and shovels (NVIDIA chips, data centers, power). ASML makes the one machine without which none of those picks and shovels can be manufactured in the first place. It sits at the very top of the funnel for the entire semiconductor industry.

I own ASML because it is one of the rare businesses with a genuine, durable, almost-unassailable monopoly on something the world needs more of every year.

Where ASML Sits in the Chain

ASML is the chokepoint at the start of the whole semiconductor supply chain. Roughly the order is: