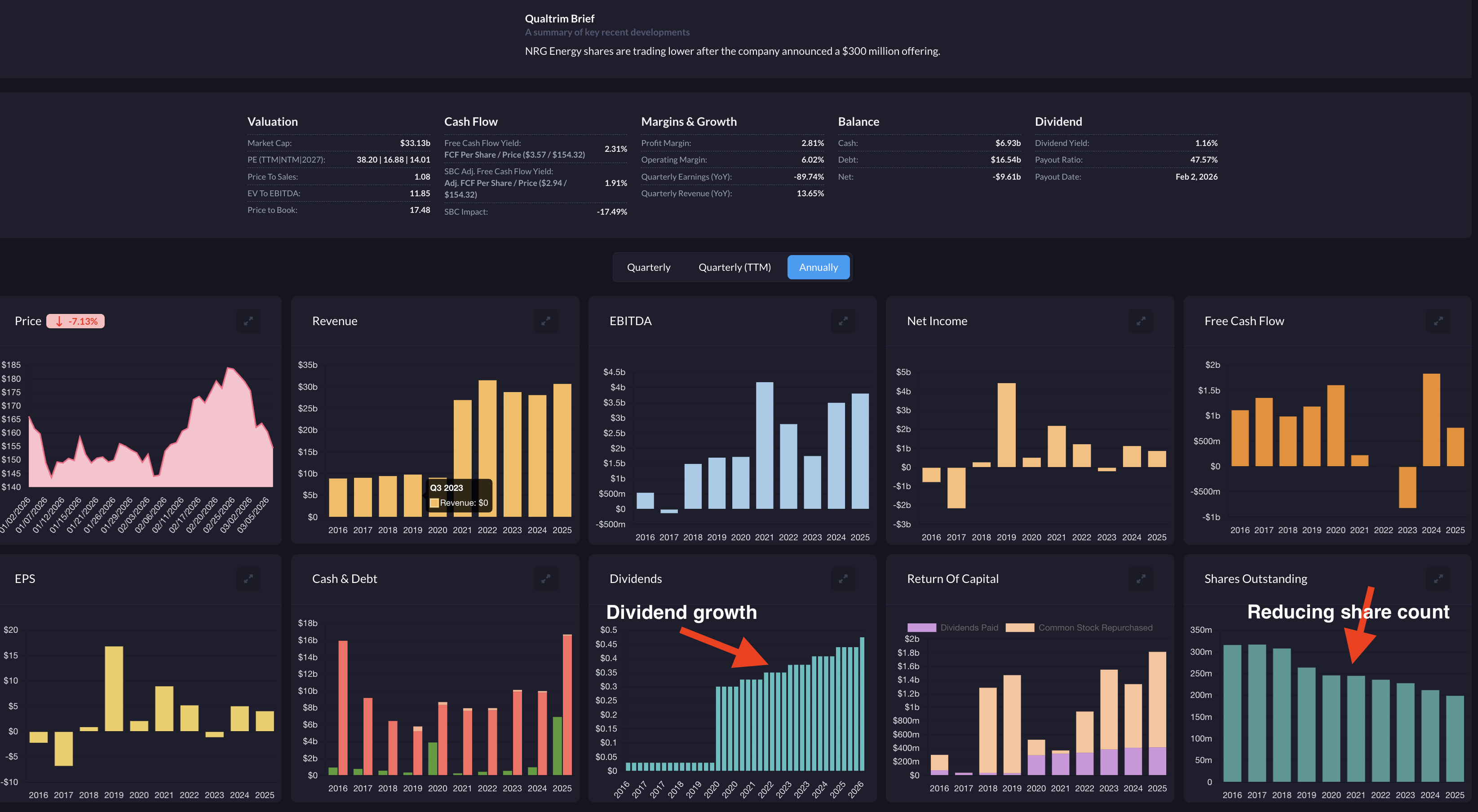

NRG Energy sells electricity and home services to roughly 8 million customers under brands like Reliant and Green Mountain Energy, and after doubling its power plant fleet to about 25 gigawatts through the LS Power deal it now owns one of the largest generation fleets in the country, right as data centers drive a sharp surge in US power demand. The stock has fallen about 25% from its 52-week high near $190 to ~$141.55, even as the company guides to double-digit earnings growth.

Catalysts

Data-center power deals (excluded from guidance): NRG has signed retail agreements with data centers that ramp from 5 MW in 2026 to 445 MW by 2032, at target pricing above $80 per MWh and retail margins above $25 per MWh. None of this upside is in the official numbers, so each new contract is incremental. Management expects to announce a large data-center agreement tied to new gas generation during 2026.

The GE Vernova and Kiewit gas build (the big multi-year one): NRG has locked up 5.4 GW of new gas-fired turbine capacity through a joint venture, with GE Vernova supplying turbines and Kiewit handling construction. The schedule: 1.2 GW in service by 2029, another 1.2 GW by 2030, and 3.0 GW more between 2030 and 2032. This is purpose-built to serve data-center demand in Texas and PJM, and securing turbine slots is itself a scarce advantage right now.

Rising PJM capacity payments: NRG is set to collect $644M in PJM capacity revenue in 2026, rising to $729M in 2027, from roughly 6,000 MW cleared at $298 to $333 per MW-day. Management notes the forward market does not yet reflect how tight supply is getting, so future auctions could clear higher.

A power-supply squeeze in its core markets: Texas electricity demand is up nearly 30% over five years, and building new generation takes years. Owning 25 GW of existing plants in ERCOT and PJM is worth more as the shortage deepens. NRG's "bring your own power" strategy pairs its generation directly with new large customers.

Aggressive buybacks into weakness: With the stock down about 25% from its high, NRG is repurchasing roughly $1.1B of shares in 2026 ($817M already done through April), which shrinks the share count and lifts per-share earnings.

Key risks

Merchant power means commodity and weather swings (the big one): A large part of NRG's profit comes from selling power at market prices, which move with electricity demand, natural-gas prices, and weather. A mild summer, a warm winter, or soft power prices can dent results, as the soft first quarter of 2026 showed. This is the core reason a power producer does not earn a High conviction rating.

Elevated leverage after a debt-funded deal: NRG paid for the LS Power assets largely with debt, and total liquidity dropped from $9.6B at the end of 2025 to $3.3B by March 2026. Net debt is now roughly 3 times earnings before interest, taxes, depreciation, and amortization, above the company's own 2.50 to 2.75x investment-grade target. They plan ~$1.1B of debt paydown in 2026 to bring it back down, but until then the balance sheet has less cushion.

Integration and a new CEO at the same time: NRG is absorbing a fleet-doubling acquisition while Robert Gaudette has just stepped in as CEO (April 30, 2026), succeeding Larry Coben. Management says integration is tracking ahead of plan, but a big merger plus a leadership change is execution risk stacked on execution risk.

The upside is promised, not delivered: The data-center contracts, the 5.4 GW gas build, and higher PJM prices are real opportunities, but most of the dollars arrive in 2029 and beyond. If demand or pricing disappoints, the bull case thins out and you are left owning a fairly leveraged merchant power company.

Regulatory and market-design risk: ERCOT and PJM rules (capacity auctions, reliability mandates, price caps) can change in ways that help or hurt merchant generators, and these decisions are outside NRG's control.

Portfolio position

3.1% of TFSA+5.77%

NRG Energy (NRG) Investment Evaluation Brief

Last updated: June 24, 2026

Price at writing:~$141.55 (June 24, 2026; the stock was volatile in June, ranging roughly $120 to $142)

Market cap: ~$29.9B

Sector: Utility / Independent Power Producer (IPP) and retail energy

Layer: Power Generation (plus retail energy supply)

Conviction: Medium (weighted score 3.65 / 5.0; expected hold 3-5 years)

Verdict: Buy under ~$150, double down under ~$125. At ~$141.55 it is in the buy zone. DCA in progress.

NRG Energy sells electricity and home services to roughly 8 million customers under brands like Reliant and Green Mountain Energy, and after doubling its power plant fleet to about 25 gigawatts through the LS Power deal it now owns one of the largest generation fleets in the country, right as data centers drive a sharp surge in US power demand. The stock has fallen about 25% from its 52-week high near $190 to ~$141.55, even as the company guides to double-digit earnings growth.

1️⃣ Summary/Snapshot

NRG is a power producer and electricity retailer trading at about 14 times next year's estimated earnings while targeting 14% annual earnings growth, with the data-center power boom as upside it has not even put in its numbers. The plan: buy under , double down under . At it is in the buy zone.

~$150

~$125

~$141.55

Cheap for the growth, with upside the company leaves out: It trades at roughly 14 times next year's estimated earnings of about $10 a share while targeting 14% yearly growth through 2030, and that target deliberately leaves OUT the data-center contracts and higher PJM capacity prices, so those are extra if they arrive. Analysts are strongly bullish (average target ~$199, about +41%).

A doubled fleet right into a power shortage: The LS Power deal (closed January 2026) doubled generation to about 25 GW, much of it in Texas (ERCOT) and the PJM region, the two markets where data-center demand is surging and new supply is scarce. Texas power use is up nearly 30% in five years.

Real cash, returned aggressively: About $3.05B of free cash flow before growth is guided for 2026, funding roughly $1.1B of buybacks, $1.1B of debt paydown, and $407M of dividends. The company repurchased $817M of stock through April alone, buying into the price weakness.

The catch is leverage and commodity swings: The acquisition was debt-funded (liquidity fell from $9.6B to $3.3B), the business is merchant power (profits move with power prices, gas prices, and weather), and a new CEO took over in April. This is why it is Medium conviction, not High.

At a Glance

Item

Detail

Verdict

Buy < ~$150 · Double down < ~$125

Current price

~$141.55 (June 24, 2026)

Base-case fair value

~$162 (+14% vs ~$141.55, June 24)

Probability-weighted fair value

~$166 (+17% vs ~$141.55, June 24)

Analyst target (avg / median)

~$199 / ~$200 (+41% / +41% vs ~$141.55, June 24)

Valuation method

Forward P/E (dividend model as floor; sector-appropriate)

Moat

Moderate (scarce generation in supply-tight markets + large retail base)

Key catalyst

Data-center power deals + rising PJM capacity prices (both excluded from guidance)

Risk to watch

Merchant/commodity swings and elevated post-deal leverage

Next earnings

~Early August 2026 (Q2; sources cite Aug 4 or Aug 12)

Valuation Summary

Scenario

Fair Value / Share

vs ~$141.55 (June 24)

Conservative

~$132

-7%

Base

~$162

+14%

Bull

~$203

+43%

Valued on next year's estimated earnings (P/E), the right lens for a power producer. The dividend-based estimate lands at only ~$47 and is shown solely as a floor, because NRG returns far more cash through buybacks than dividends. See Section 6.

Notable Analyst Price Targets

Firm

Rating

Price Target

Date / Notes

Street high

n/a

$267

Most bullish estimate

Average

Buy

~$199

14 Buy / 1 Sell

Median

n/a

~$200

Goldman Sachs

Buy

(not broken out)

Recent initiation/reaffirm

Wells Fargo

Buy

(not broken out)

Reaffirmed several times, June 2026

Street low

n/a

$99

Bear case (commodity/merchant skeptics)

Where to Find More Detail

Section 4 (Plain-English): What NRG does and how the data-center boom flows to it.

Section 6 (Quantitative): Why this is valued on earnings rather than projected cash flow, the scenario math, and the dividend floor.

Section 7 (Six-Category Evaluation): The scored framework behind the Medium rating.

Section 8 (Strategy): The buy and double-down rules.

2️⃣ Catalysts

Data-center power deals (excluded from guidance): NRG has signed retail agreements with data centers that ramp from 5 MW in 2026 to 445 MW by 2032, at target pricing above $80 per MWh and retail margins above $25 per MWh. None of this upside is in the official numbers, so each new contract is incremental. Management expects to announce a large data-center agreement tied to new gas generation during 2026.

The GE Vernova and Kiewit gas build (the big multi-year one): NRG has locked up 5.4 GW of new gas-fired turbine capacity through a joint venture, with GE Vernova supplying turbines and Kiewit handling construction. The schedule: 1.2 GW in service by 2029, another 1.2 GW by 2030, and 3.0 GW more between 2030 and 2032. This is purpose-built to serve data-center demand in Texas and PJM, and securing turbine slots is itself a scarce advantage right now.

Rising PJM capacity payments: NRG is set to collect $644M in PJM capacity revenue in 2026, rising to $729M in 2027, from roughly 6,000 MW cleared at $298 to $333 per MW-day. Management notes the forward market does not yet reflect how tight supply is getting, so future auctions could clear higher.

A power-supply squeeze in its core markets: Texas electricity demand is up nearly 30% over five years, and building new generation takes years. Owning 25 GW of existing plants in ERCOT and PJM is worth more as the shortage deepens. NRG's "bring your own power" strategy pairs its generation directly with new large customers.

Aggressive buybacks into weakness: With the stock down about 25% from its high, NRG is repurchasing roughly $1.1B of shares in 2026 ($817M already done through April), which shrinks the share count and lifts per-share earnings.

3️⃣ Key Risks

Merchant power means commodity and weather swings (the big one): A large part of NRG's profit comes from selling power at market prices, which move with electricity demand, natural-gas prices, and weather. A mild summer, a warm winter, or soft power prices can dent results, as the soft first quarter of 2026 showed. This is the core reason a power producer does not earn a High conviction rating.

Elevated leverage after a debt-funded deal: NRG paid for the LS Power assets largely with debt, and total liquidity dropped from $9.6B at the end of 2025 to $3.3B by March 2026. Net debt is now roughly 3 times earnings before interest, taxes, depreciation, and amortization, above the company's own 2.50 to 2.75x investment-grade target. They plan ~$1.1B of debt paydown in 2026 to bring it back down, but until then the balance sheet has less cushion.

Integration and a new CEO at the same time: NRG is absorbing a fleet-doubling acquisition while Robert Gaudette has just stepped in as CEO (April 30, 2026), succeeding Larry Coben. Management says integration is tracking ahead of plan, but a big merger plus a leadership change is execution risk stacked on execution risk.

The upside is promised, not delivered: The data-center contracts, the 5.4 GW gas build, and higher PJM prices are real opportunities, but most of the dollars arrive in 2029 and beyond. If demand or pricing disappoints, the bull case thins out and you are left owning a fairly leveraged merchant power company.

Regulatory and market-design risk: ERCOT and PJM rules (capacity auctions, reliability mandates, price caps) can change in ways that help or hurt merchant generators, and these decisions are outside NRG's control.

4️⃣ Plain-English Business Explanation

What NRG actually does

NRG has two connected businesses. First, it is one of the largest sellers of electricity and natural gas to homes and businesses in the US, serving roughly 8 million customers under brands like Reliant, Green Mountain Energy, and Direct Energy, plus the Vivint smart-home business. Second, after the LS Power deal it owns about 25 GW of power plants (mostly natural gas), making it also one of the largest power generators in the country.

Owning both the power plants and the customer relationships is the point. NRG can generate electricity and sell it straight to its own customers, capturing margin at both ends and hedging itself: when power prices spike, its generation profits rise even if its retail costs do too.

How it makes money

Three main ways: Selling electricity and gas to retail customers at a margin, selling power from its plants into wholesale markets at market prices, and collecting "capacity payments" (money grid operators like PJM pay generators just to be available when demand peaks). The retail business is steadier; the generation business is more profitable but swings with commodity prices and weather.

Who uses it: Millions of households and businesses for their electricity and gas, plus large new power buyers, most importantly data-center operators that need reliable, around-the-clock power and are signing long-term deals.

How it connects to AI

This is the heart of the thesis, and unlike most names in the portfolio it is about supplying the AI boom rather than building the computers.

AI data centers consume enormous amounts of electricity, and they cluster in places with available power, increasingly Texas (ERCOT) and the PJM region (the mid-Atlantic and Midwest). Both markets are running short of power because demand is climbing far faster than new plants can be built. NRG already owns 25 GW of generation in exactly these markets. That makes its existing plants more valuable (scarcity pushes up both energy and capacity prices), and it lets NRG sign premium long-term contracts to power new data centers, and even build new gas plants (the GE Vernova and Kiewit venture) dedicated to them.

The important nuance: NRG's demand does NOT depend on AI alone. Electrification, manufacturing moving back onshore, population growth, and electric vehicles are all lifting power demand too. AI is the accelerant, not the whole story, which gives the thesis some insulation if AI spending cools.

A simple analogy

Think of NRG as owning both the gas stations and the refineries in a fast-growing boomtown where no one is allowed to build new refineries quickly. As more people and businesses pour in (data centers being the biggest new arrivals), the fuel everyone already depends on gets more valuable, and NRG sells it at both the pump and the wholesale level. The risk is that fuel prices themselves swing around, and the company borrowed heavily to buy a second refinery.

Why the market has not warmed up to it

Merchant power stocks are volatile and investors discount them for commodity and weather risk.

The big debt taken on for the LS Power deal makes some investors cautious until leverage comes down.

A soft first quarter and a new CEO created near-term uncertainty.

Much of the data-center upside is years away, so the market is waiting for signed contracts before paying for it.

Reading: A strongly bullish consensus, and unusually so. The average (~$199) and median (~$200) sit right on top of each other, so the average is not skewed by one outlier. But the range is very wide ($99 to $267), which is the market telling you this is a leveraged, commodity-sensitive business where the outcome depends a lot on power prices and whether the data-center upside lands. The bulls are pricing the upside that guidance excludes; the lone bear is pricing a commodity downturn.

Why this is valued on earnings, not projected cash flow

A power producer like NRG is best valued on its earnings and dividend, the standard yardsticks for this kind of company. The projected-cash-flow approach used for many growth businesses does not fit well here. NRG's headline cash measure (free cash flow before growth) is large, roughly $14 per share, but much of that cash is plowed straight back into building new plants and paying down debt, and that reinvestment is what powers the company's growth in the first place. You cannot both spend the cash on growth and hand it all to shareholders, so projecting it forward while also growing it overstates the value wildly: it implies a price well above even the most bullish analyst. The cleaner method for a business like this is to value its earnings, use the dividend as a floor, and treat the cash-flow yield as a supporting check. That is what the scenarios below do.

Forward P/E scenarios

NRG's earnings are guided at about $8.90 per share for 2026, and the company targets 14% per-share growth, which would put 2027 around $10 per share (an estimate, not company guidance; independent analyst figures cluster near $10 to $11). The scenarios value that estimated ~$10.15 across a range of price-to-earnings multiples. For reference, the stock trades at about 14 times that figure today, a low multiple for a company growing 14%, which is the core of the bull argument.

Inputs:

Price (June 24, 2026): ~$141.55

2026 adjusted EPS (company guidance): ~$8.90

2027 adjusted EPS (estimated: 2026 guidance grown at the 14% target): ~$10.15

Multiple range: 12x (deep conservative) to 22x (deep bull); central cases 13x / 16x / 20x

Cross-check: Analyst average $199 implies about 19.6x the estimated 2027 earnings

For a power producer the live question is less what it earns than what multiple the market is willing to pay, so each scenario below holds the estimated 2027 earnings (~$10.15) fixed and varies the multiple across a small band. The central row in each table is the headline case; the rows around it show how fair value moves if the market pays a little more or less. This is the P/E analog of varying the discount rate in a cash-flow model.

Valuation Summary

Scenario

Fair Value Range / Share

vs ~$141.55 (June 24)

Conservative

~$122 to ~$142 (central ~$132)

-14% to +0%

Base

~$152 to ~$173 (central ~$162)

+7% to +22%

Bull

~$183 to ~$223 (central ~$203)

+29% to +58%

Conservative (central 13x on ~$10.15 EPS)

Growth comes through, but the market de-rates the stock slightly: merchant and leverage risk weigh on the multiple. Modest downside on price, offset by the dividend and the buyback.

P/E Multiple

2027E EPS (est.)

Fair Value / Share

vs ~$141.55 (June 24)

12x

~$10.15

~$122

-14%

13x (central)

~$10.15

~$132

-7%

14x

~$10.15

~$142

+0%

Base (central 16x on ~$10.15 EPS)

A modest re-rating as the balance sheet de-levers and the growth proves durable. This is the central case.

P/E Multiple

2027E EPS (est.)

Fair Value / Share

vs ~$141.55 (June 24)

15x

~$10.15

~$152

+7%

16x (central)

~$10.15

~$162

+14%

17x

~$10.15

~$173

+22%

Bull (central 20x on ~$10.15 EPS)

The data-center contracts and higher PJM prices land, leverage falls, and the market values NRG closer to its fast-growing peers.

P/E Multiple

2027E EPS (est.)

Fair Value / Share

vs ~$141.55 (June 24)

18x

~$10.15

~$183

+29%

20x (central)

~$10.15

~$203

+43%

22x

~$10.15

~$223

+58%

Probability-weighted fair value: Weighting 20% conservative / 55% base / 25% bull on the central multiples (13x / 16x / 20x) gives ~$166 (+17% vs ~$141.55). The analyst average ($199) sits between the base and bull cases, so the Street is a bit more optimistic than this central estimate.

Dividend-based floor (context only)

Valuing the $1.90 per share annual dividend on its own (grown at 8% then 4%, discounted at 9%) yields only about $47. This is NOT a real estimate of value; it is a floor that exists because NRG deliberately returns most of its cash through buybacks, not dividends, so a dividend-only method cannot see the roughly $1.1B of annual repurchases. It is shown only to confirm that for this company a dividend-based approach understates value badly, which is why the earnings method leads.

Free-cash-flow yield (context only)

NRG's free cash flow before growth of ~$3.05B on a ~$29.9B market value is roughly a 10% yield, which is high and supports the cheap-for-the-growth view. The caveat already noted: a chunk of that cash is reinvested to drive the growth and to pay down debt, so it is not all distributable today.

Stock-based compensation

Immaterial. NRG's stock-based pay runs on the order of $100M a year against $2-3B of free cash flow before growth and $1B+ of buybacks, far below the level that would require an adjusted view. No stock-comp adjustment is needed here.

Interpretation and stress test: On earnings, NRG is cheap for its growth, and the data-center upside is genuinely free in the numbers. The honest worry is the multiple: a power producer with elevated leverage may simply not get re-rated, in which case you earn the growth and the buyback but little multiple expansion. Stress test: If 2027 earnings come in at $9.00 instead of the estimated $10.15 (growth disappoints) and the multiple stays at 13x, fair value is about $117, roughly 17% below today. The balance sheet, not the income statement, is the thing that could turn a disappointment into something worse, which is why leverage is the number to watch.

7️⃣ Six-Category Evaluation

This is the scoring framework that produces the Medium conviction rating at the top. Six areas are each scored 1.0 to 5.0, then weighted using the Utility/IPP weighting (which puts more emphasis on the balance sheet than the tech weighting does), and the weighted average sets the conviction tier.

Category 1, Quantitative: 4.0

Genuinely cheap for the growth: about 14x estimated 2027 earnings for a company targeting 14% per-share growth, with analysts seeing roughly 40% upside and an ~10% cash-flow yield. Why not higher: The value depends on the market assigning a higher multiple, and merchant-power stocks are routinely discounted; there is no guarantee of a re-rating. Why not lower: The valuation is cheap on multiple measures at once, and the analyst support is broad (14 Buy, 1 Sell).

Category 2, Qualitative: 4.0

A strong, multi-pronged demand story: a doubled generation fleet positioned in the two tightest US power markets, signed data-center contracts ramping to 445 MW, a 5.4 GW gas build locked up with GE Vernova and Kiewit, rising PJM capacity payments, and Texas demand up ~30% in five years. The revenue/volume driver (rising power demand) is only partly AI-dependent: electrification, onshoring, and population growth lift it too, which insulates the base case somewhat from an AI slowdown. The re-rate driver (a higher earnings multiple) leans more on the data-center story landing. Why not higher: Much of the biggest upside arrives in 2029 and later and is not yet contracted in full; it is a credible plan, not banked results. Why not lower: The tailwinds are real, diverse, and already showing up in capacity revenue and early contracts.

Category 3, Category Classification: 3.5

A merchant power producer paired with a retail energy and home-services business, with a growth overlay from data centers. It fits the Utility/IPP bucket cleanly and is best owned as common stock for several years. Why not higher: The merchant/commodity core makes earnings less predictable than a regulated utility's. Why not lower: The integrated retail-plus-generation model is coherent and partially self-hedging, and the classification is unambiguous.

Category 4, Bottleneck/Moat: 4.0

A real, if moderate, moat. NRG owns about 25 GW of generation in ERCOT and PJM, markets where new supply is scarce and slow to build, so its existing plants are a genuine bottleneck during a power-demand surge. It also has secured turbine slots (themselves in short supply) and a large retail customer base with brand and switching friction. Why not higher: Merchant power is ultimately a commodity; the moat is scarcity-and-scale, not a durable pricing monopoly. Why not lower: Owning hard-to-replace generation in supply-constrained markets during a structural demand boom is a strong position that competitors cannot quickly copy.

Category 5, What Could Go Wrong: 3.0

Several material risks: commodity and weather swings in the merchant business, elevated leverage after a debt-funded acquisition, integration of a fleet-doubling deal, a brand-new CEO, and regulatory dependence on ERCOT and PJM rules. The partial AI-independence of demand (electrification, onshoring) gives some insulation from the portfolio's biggest shared risk, an AI-spending slowdown, but does not offset the commodity and leverage exposure. Why not higher: These are real, simultaneous risks, and the leverage reduces the margin for error. Why not lower: The retail business partly hedges the generation business, demand is structurally rising, and management is prioritizing debt paydown, so none of the risks looks existential.

Category 6, Balance Sheet Quality: 3.0

The weak spot. The LS Power deal was debt-funded; liquidity fell from $9.6B to $3.3B, and net debt sits around 3x earnings, above the company's own 2.50 to 2.75x investment-grade target. Why not higher: Leverage is elevated and the cushion is thinner than before the deal. Why not lower: The company generates strong cash flow, has reaffirmed an investment-grade target, refinanced to extend maturities and cut interest, and has earmarked ~$1.1B for debt paydown in 2026; the leverage is high but being actively managed down.

Weighted Score Calculation

Category

Score

Weight (Utility/IPP)

Contribution

1. Quantitative

4.0

20%

0.80

2. Qualitative

4.0

15%

0.60

3. Category Classification

3.5

10%

0.35

4. Bottleneck/Moat

4.0

25%

1.00

5. Risk

3.0

15%

0.45

6. Balance Sheet

3.0

15%

0.45

TOTAL

100%

3.65

Hard-fail check: No category at 1.0 in Quantitative, Risk, or Balance Sheet. No hard fail. Interpretation: 3.65 sits in the Medium tier (3.0-3.9), at the higher end. A solid, sensibly-sized holding, with the balance sheet and commodity exposure being what keep it out of the High tier.

8️⃣ Strategy

Buy under ~$150. That is below the base-case fair value (~$162) and well below the analyst average (~$199), so it leaves a margin of safety. Accumulate gradually via DCA. At ~$141.55 it remains in the buy zone.

Double down under ~$125. Roughly double the cash per buy. This is near the recent 52-week low ($120.11), where the price/earnings multiple compresses toward 12x and the risk/reward improves further.

One condition: Keep buying only while leverage is trending down and the data-center and PJM catalysts stay on track. If net debt climbs instead of falling, or a major contract or the gas build slips badly, pause and reassess.

Holding period: 3-5 years, to let de-leveraging, the data-center contracts, and the new gas capacity play out.

Reduce / exit triggers:

Trigger

Action

Net debt rises toward/above ~3.5x EBITDA instead of falling

Pause adds; reassess

Power/gas price collapse cuts generation margins for multiple quarters

Reduce; thesis weakening

Data-center deals or the GE Vernova/Kiewit build slip materially

Reassess the upside case

The multiple re-rates to ~19-20x (toward analyst targets)

Trim into strength; upside largely captured

9️⃣ Open Questions

What is NRG's exact net debt and net-debt-to-EBITDA after the LS Power funding and the April refinancing? (The ~3x figure here is an estimate and should be confirmed against the latest 10-Q balance sheet.)

When will the large data-center power agreement management flagged for 2026 actually be signed, and at what size and price?

How fast is leverage actually coming down quarter by quarter, and does the company hold its investment-grade rating through the de-leveraging?

Does the soft Q1 reverse over the summer (NRG's seasonally strong period), confirming full-year guidance, or does weather/commodity weakness persist?

Is the 2026 adjusted EPS guidance (~$8.90) confirmed against the latest filing? Some data aggregators show higher forward figures (~$10-11) that appear to fold in the upside NRG excludes from guidance.

Research for personal use. Not investment advice. Verify pricing, share count, net debt, guidance, and material developments through primary sources before any transaction. Power-producer earnings are sensitive to commodity prices and weather, and the valuation here depends heavily on the earnings multiple the market assigns and on leverage continuing to decline.